For a functioning and harmonious socio-economic system, this author believes that there needs to be a good balance among three interrelated factors: economic efficiency/growth, resilience, and social equity/sustainability.

This article seeks to take a critical view of the current ESG reporting mechanism. It will discuss a new ESG model based on the Integrated Conceptual Framework of Responsible Management (Simon S.M. Ho 2020) and take three core dimensions into account: Stakeholders, Ethics, and Sustainability (or Sustainable Values). It recommends that any such mechanism should aim to first uncover the extent to which management acts ethically toward different stakeholders, and optimise their respective sustainable values.

In recent years, corporate leaders, academics, and institutional investors have increasingly favoured a more inclusive model of capitalism, one which benefits other stakeholders besides shareholders. They have agreed to reshape the indulgent capitalism, as well as redefine the nature, purposes, and responsibilities of corporations. Corporations are important social institutions that should abide by social contracts promulgated several hundred years ago, and thus, optimise the sustainable values of different interdependent stakeholders (not just maximise shareholders’ values, MSV). Businesses shouldn’t be causing social problems, but rather solving them by creating economic and social value.

Market players have gradually adopted “responsible management” concepts and practices to reverse the MSV trend. Among other similar initiatives (corporate social responsibility [CSR], creating shared values, benefit corporations, conscious capitalism, social impact investment, etc.), many companies spend considerable resources on environment, social and governance (ESG) activities.

ESG practices have potential environmental and societal benefits; and companies adopt ESG metrics for more efficient resource allocation, better risk management, and more sustainable corporate growth. Theoretically, investing in ESG (now ESG factors are considered in over 25% of all investment assets) may lead to lower corporate returns in the short run, but would produce more long-term sustainable value for stakeholders.

However, ESG reporting requirements, with multiple complex standards and metrics, are also a source of debate. As many inherent concerns regarding ESG reporting have not been addressed, it is difficult to determine to what extent piecemeal revisions of the requirements by the stock exchange or regulatory bodies can significantly improve the cost effectiveness of ESG reporting, especially in achieving social and environmental impact.

Unfortunately, current ESG reporting lacks a robust common conceptual framework that links different terms and concepts together. It is also flawed in clarity regarding its purpose, elements and limitations. Concerns and insights mentioned above highlight the need for a revised ESG model that embodies the core values of “responsible management”.

This article seeks to take a critical view of the current ESG reporting mechanism. It will discuss a new ESG model based on the Integrated Conceptual Framework of Responsible Management (Simon S.M. Ho 2020) and take three core dimensions into account: Stakeholders, Ethics, and Sustainability (or Sustainable Values). It recommends that any such mechanism should aim to first uncover the extent to which management acts ethically toward different stakeholders, and optimise their respective sustainable values.

Author argues that current ESG reporting lacks a robust common conceptual framework that links different terms and concepts together. (Shutterstock)

Some Problems with Existing ESG Reporting

While recognising the popularity and general acceptance of ESG, the concept so far lacks a robust theory and conceptual framework. Consequently, ESG is arguably a loose and convenient buzzword which begs clarity regarding its definition, purpose, assumption, elements, and limitations.

There has never been any serious discussion in either the market or literature regarding why the three domains “E”, “S” and “G” are put together, why in this particular order, nor how they are interrelated. Consequently, many individuals confuse it with terms such as CSR, benefit corporations, creating shared values, conscious capitalism, or impact investment.

Several misunderstandings have also been caused by some ESG terms. For instance, does “Environment” = “Sustainability”? “Social” = “CSR”? “ESG” = “CSR” = “Sustainability”? ESG compliance = ESG ratings? = ESG impacts? = ESG investment returns? And good financial returns = good values to different stakeholders?

By lacking a rigorous integrated conceptual framework for responsible management, the major problem with existing ESG reporting and other similar concepts is that it is not based on a company’s purpose and responsibilities, i.e. optimising sustainable values to different stakeholders.

Currently, most ESG reports place more focus on “E” KPIs, much less on “S” and “G”. However, the HKCFA Institute survey shows that 50% of investors consider “E”, 40% consider “S”, and 65% consider “G”. Most ESG reports focus on “environmental sustainability” and on investors’ information needs, and demonstrate little concern for business ethics and responsibilities to different stakeholders. The dimension of “Social” (S) is clearly too broad and too loose. There are also difficulties in measuring “S”, as “E” and “G” are more objective, and “S” is more subjective.

Currently, most ESG reports place more focus on E KPIs, much less on S and G. (Shutterstock)

A Reformed ESG Model Adopting Responsible Management Concepts

To address the current shortcomings, the first step in reforming the ESG reporting model is to identify a sound and comprehensive conceptual framework.

We believe that corporations are important social institutions that have the capacity to benefit various stakeholders, including the environment and society. In recent years, some business and academic leaders have suggested redefining the purpose of corporations from the perspective of social contracting. That is, companies, which enjoy privileges such as limited liability, unlimited life and independent legal-person status, should implicitly agree to bear responsibilities for various interdependent stakeholders. Thus, corporate leaders should not concentrate solely on shareholders’ interests, but should optimise sustainable value for all stakeholders upon whom the corporations’ existence is dependent. In other words, corporations need to balance the interests of all major stakeholders and aim for sustainable growth.

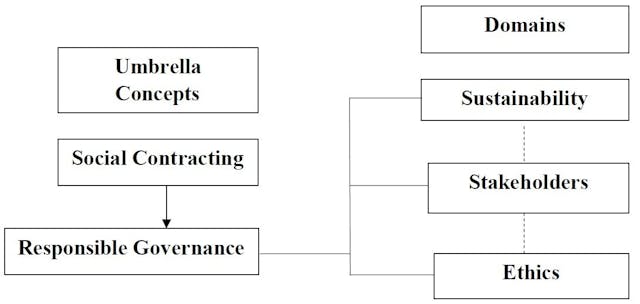

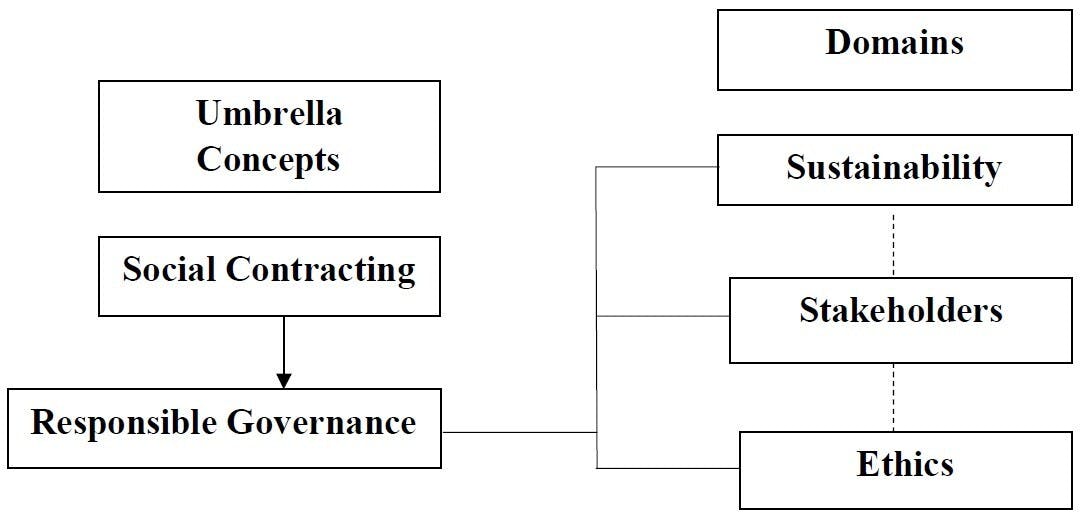

We therefore advocate for a reformed ESG model based on the integrated conceptual framework of responsible management developed by this author in 2020 (see attached exhibit). This framework stems from the umbrella concept of social contracting and examines the core values of responsible management.

In the integrated framework, three core domains are identified: stakeholders, ethics, and sustainability. These three domains are put under “Governance” which provides the overall corporate direction and leadership for “responsible management”. A brief definition of each of these three domains is given below:

1. Stakeholders: This emphasises the disclosure of the sustainable value created for each of the stakeholder groups, including shareholders/investors, senior management, employees, customers, suppliers, creditors, community, regulators and the government.

2. Ethics: The existing model pays little attention to “inner well-being” or ethics, which is the foundation for responsible management behaviour. Ethics represent the moral principles, values or conscience that govern a company’s behaviour to avoid harming (before talking about creating values) different stakeholders, and are also represented by the implementation of appropriate business policies and practices that are not obliged by law.

3. Sustainability: This represents meeting the needs of this generation without compromising those of future generations. Sustainability is centred on the core concept of the triple bottom line, i.e., the goals of “people, planet, and profit” (John Elkington). It enables organisations to take a longer-term perspective and evaluate the future consequences of decisions.

Together with the umbrella concepts of social contracting, these different domains are complementary, mutually reinforcing but distinct, each with their own core concepts and execution. For ESG reporting, we can combine these three domains into one measurement: the sustainable values created for each of the different stakeholders.

Besides environment (E) and governance (G) performance indicators in the existing model, the “S” or “Social” domain of the existing ESG model is arguably broad and therefore confusing, as it consists of a number of loose reporting elements such as human rights, labour laws, employee training, equal opportunities and diversity, corruption prevention, occupational health and safety, product liability, supplies chain management, charity and volunteering, and community investment, etc., which do not necessarily relate to each other.

A recent USA survey showed that investors who primarily rely on “Social” disclosures/ratings have a much lower returns than investors who relied on “E” or “G”. Currently, the expectations and information needs of different stakeholders are not systematically addressed or reported. We advocate for “S” to represent “Stakeholders” instead of the broad and potentially confusing “Social”.

The existing “Social” indicators should be re-classified according to the extent of ethics practiced, and the amount of sustainable values created (or reduced) for each of the following stakeholder groups: shareholders, employees, senior management, customers, suppliers, creditors, community, and government and regulators. Together, this would lead to the ultimate sustainability of “people, planet and profit” (the 3Ps) as described in the earlier section.

The reformed ESG reporting model functionally links stakeholders, ethics, and sustainability, and this robust framework should effectively address many major shortcomings of the existing practice.

The existing Social indicators should be re-classified. (Shutterstock)

Measuring ESG, Corporate and Investment Performance

About 65 years ago, management guru, Peter Drucker, made it clear that business’ “first responsibility is to operate at a profit”, so as to fulfil its role as “the wealth- creating and wealth-producing organ of our society”. But Drucker also believed that social responsibility would be the highest expectations of business purpose. Therefore, a business should create both economic and social values.

But will firms with a high ESG score/rating outperform their peers or the market (i.e. an alpha return)? There has been little clear empirical evidence. One reason being that there are almost no common agreeable research frameworks, variables, weightings, and measurements. It may also be due to low information value-relevance or “greenwashing” of ESG (especially “S”) disclosures.

Another major reason is that high ESG compliance/ratings do not imply true ESG impact. According to a Bloomberg study report, there is solid evidence that major firms with true and significant social/environment impacts lead to visible alpha investment returns even though their ESG ratings are low, once again demonstrating that ESG ratings do not equal ESG impact.

We understand that many short-term investors still buy stocks with low ESG ratings, as “doing good” and “doing well short-term” and are often incompatible. Therefore, a firm has to identify its ESG strategy and tell its “good ESG stories”. It needs to ensure that ESG investment can start generating continuous cash inflow in a few years’ time, and it needs to have a good balance between short-term return pressure, and long-term values.

ESG is not the entire representation of corporate success or effectiveness. Besides ESG, corporate performance involves factors such as leadership, culture, strategy, risk management and innovation. We also measure the sustainable value created for each stakeholder, and the different stakeholders’ assessment of management performance. A balanced-score-card type with multi-dimensional (both tangible and intangible, financial and non-financial, economic and social) measurements is needed for effective assessment.

Towards a Stakeholder-based Green Economy

Across the globe, it is evident that the current ESG reporting model has greatly fallen short of the society’s expectations. Different stakeholders are desperately waiting for new direction on this matter.

This article lays out a new ESG model, the “Environment, Stakeholders, and Governance” model, with the same acronym “ESG”, based on the integrated conceptual framework of responsible management described. “S” disclosure standards/KPIs should be re-classified/reported by different groups of stakeholders. This robust model should effectively address some major shortcomings of the existing practices.

Universities should nurture future purposeful and responsible leaders who pursue the optimisation of the sustainable values of different stakeholders. Only then can we truly move towards more prosperous, resilient, and sustainable stakeholder-based green capitalism.

It is time to recalibrate. The ESG reform needs to begin today.

美國西雅圖華盛頓大學管理學與心理學文學士、英國倫敦經濟政治學院資訊系統學碩士、英國百蘭福特大學會計與財務學哲學博士。曾獲頒英聯邦學人(Commonwealth Scholar)銜,現為英國、澳洲與加拿大註冊會計師。 2009至2014年擔任澳門大學副校長(學術)。2004至2009年任香港浸會大學工商管理學院院長兼公司管治與金融政策研究中心主任。1995至2002年任香港中文大學會計學院院長/教授。現為Asian Journal of Business Ethics(《亞洲商業倫理學報》)編輯、Journal of Business Ethics編委。公共服務方面,現任香港廉政公署社區關係市民諮詢委員會主席和貪污問題諮詢委員會成員、香港企業管治論壇主席、香港童軍總會訓練委員會副主席、中國高等教育學會理事、香港玉山科技協會理事、香港–東盟經濟合作基金會理事,香港學者協會香江學者計劃學術委員會委員,以及多個國際團體的顧問。首位華人獲國際機構美國亞斯平學院 (Aspen Institute)頒發學界先鋒獎(Faculty Pioneer Award)。自2014年3月中出任香港恒生大學校長。