香港黃金中央清算及結算系統正式啟動試運行,對香港特區的長遠發展具深遠影響,當下香港正籌備首份本地五年發展規劃。

這套黃金中央結算交收系統包含兩大核心舉措:一是推出滬港黃金「實物聯通」首階段互聯互通機制;二是全新設立HAU黃金定價指標,專為香港市場打造專屬黃金價格基準。

政府同步規劃一系列配套發展舉措:擴充黃金存儲與精煉產能、豐富黃金投資產品體系、研究推出稅務優惠、配套相關保險安排、放寬強積金配置黃金ETF的彈性,並推動成立黃金行業協會,建立制度化行業治理架構。

財政司司長陳茂波明確指出,國家「十五五」規劃明確支持香港搭建大宗商品交易生態。由此可見,香港推出黃金中央結算交收系統,是特區政府積極回應中央規劃部署與政策期望的重要舉措。他又稱,成熟的黃金交易生態將拓寬香港金融市場的廣度與深度,為本地及環球投資者創造更多投資機遇,為香港金融業持續繁榮揭開全新篇章。

搭建可擴容、一體化的黃金交易基建

財經事務及庫務局局長許正宇亦指,政府的長遠目標是打造一套兼具可擴容性、一體化特徵的綜合黃金交易平台,為本地及全球市場參與者提供一站式服務,涵蓋結算交收、兩地市場互聯互通、價格發現、黃金存儲、風險管理與配套保險等全鏈路功能。

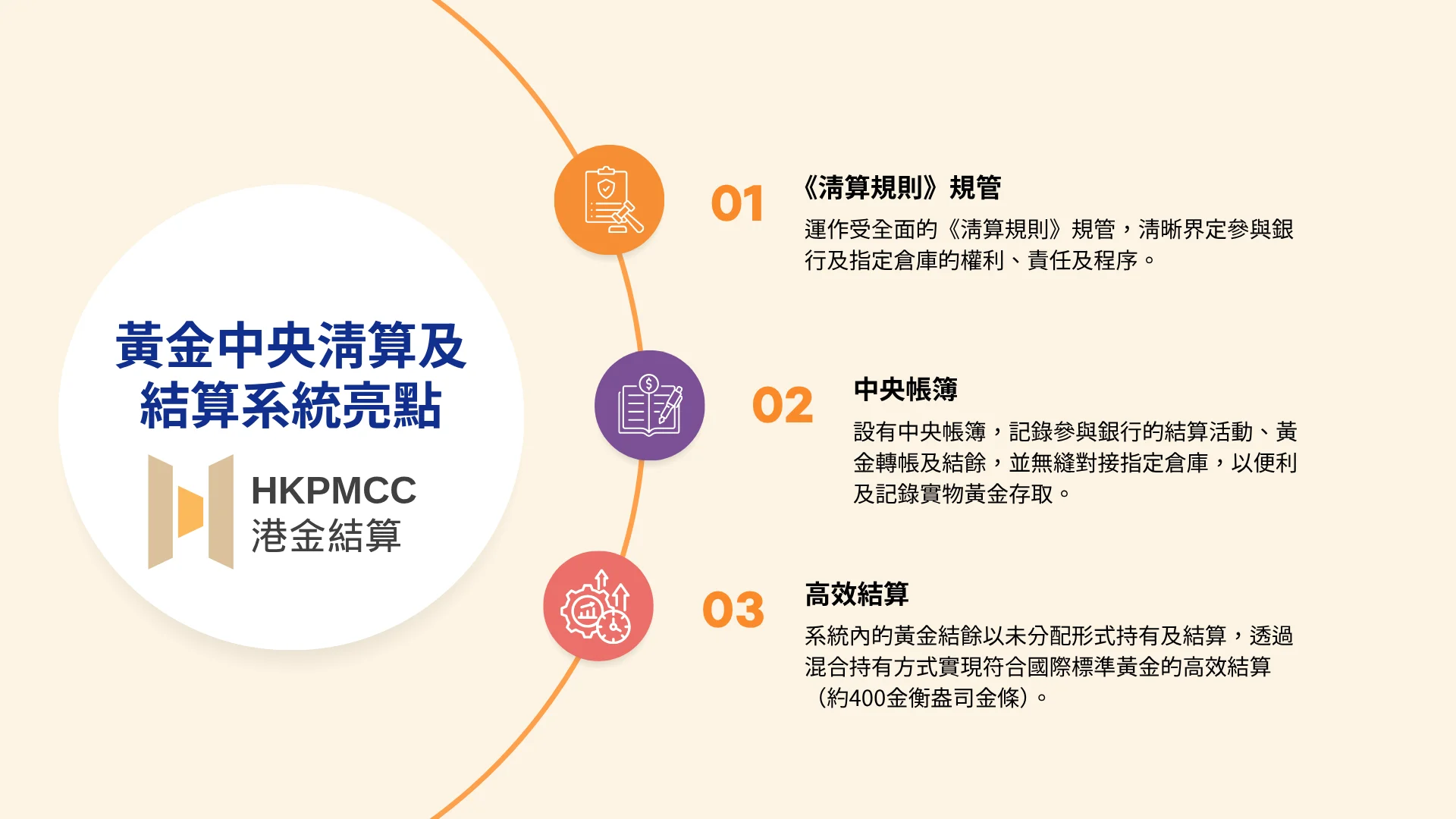

全新黃金中央清算及結算系統設立中央帳簿,統一記錄交收紀錄、黃金轉移、參與銀行持倉餘額,同時處理黃金存提業務。合資格交收標的為符合國際規格的400盎司標準金條。

包括農業銀行香港分行、澳新銀行、中國銀行(香港)、建設銀行(亞洲)、花旗香港、工銀亞洲、摩根大通、渣打香港、滙豐及瑞銀等11家銀行成為首批系統參與機構。

拓寬與內地互聯互通渠道、豐富投資品類

行政長官李家超在固定收益及貨幣峰會暨債券通論壇上表示,首階段推出的滬港黃金「實物聯通」由香港與上海黃金交易所聯合搭建,參與機構可透過該機制,在滬港兩地市場靈活調配黃金持倉完成交易結算。據李家超介紹,現已有三家銀行接入該互通機制,實現黃金雙向調撥。

與會的中國人民銀行行長潘功勝亦同時公布多項中央惠港金融政策:債券通南向投資額度提升六成、豐富內地債券產品體系,拓寬兩地雙向投資渠道,可視為香港回歸29周年後中央送出的金融政策紅利。潘功勝透露,債券通年度南向投資淨額度由現有5000億元人民幣上調至8000億元;與此同時,國家外匯儲備會持續加大在港資產配置規模,帶動香港資本市場發展。

港交所亦優化美元黃金期貨合約,並在上海黃金交易所支持下,規劃推出人民幣計價黃金期貨產品。此外,港交所與彭博合作推出全新HAU黃金定價指標,作為香港黃金交易與交收的專屬價格基準。

鞏固香港大宗商品超級連接者定位

與此同時,金管局總裁余偉文見證港交所與跨境銀行間支付清算系統(CIPS)簽署合作備忘錄。CIPS是央行搭建的跨境人民幣支付清算核心渠道,本次合作具重大經濟價值,可加速香港債券與外匯市場發展,進一步打穩香港全球領先離岸人民幣中心地位。

全新黃金中央清算及結算系統的設立,對香港自身發展、香港與內地的經貿聯繫,兼具經濟與戰略雙層重大意義。

第一,經濟層面:進一步鞏固香港金融與資本市場實力,為全球投資者提供多元化黃金投資工具。政府規劃將黃金存儲總容量擴至2000噸,提升跨境實物黃金交收效率,依託完善的黃金交易生態,強化香港全球重要金融、貨幣及黃金交易中心的地位。

第二,重塑香港作為連接內地與全球的大宗商品超級樞紐,深化與上海黃金交易所的協同。香港本已是國家核心離岸人民幣交易樞紐,黃金交易與人民幣國際化將形成雙向帶動效應,互相促進規模增長。

第三,發展政治經濟:香港金融與貨幣體系是中國對外開放、現代化建設的重要窗口,黃金交易中心的落地,將提升香港對內地經濟發展的戰略價值。

發揮一國兩制獨特比較優勢

換言之,香港持續作為國家推進人民幣國際化、拓展全球黃金交易、落實一帶一路倡議的關鍵經濟橋樑,依託本地成熟金融、資本與黃金交易平台釋放制度紅利。

第四,正如陳茂波所言,香港黃金結算系統的落地,充分呼應國家「十五五」規劃要求:中央期望香港承擔更多經濟職能、拓展大宗商品交易生態。透過充分發揮香港法律體系、國際金融中心、全新黃金結算基建的綜合比較優勢,一國兩制下香港的發展空間將進一步拓寬。

第五,近年中央持續鼓勵香港對外拓展國際合作,例如設立國際調解院、特區官員出訪中亞、中東爭取外來直接投資,足見中央全力釋放香港法律與經濟潛力。在一國兩制框架下,香港市場主導的經濟體制,承擔連接內地與全球市場的雙向橋樑角色,本次黃金結算中心落地、與上海黃金交易所聯動,正是「對外聯通、對內協同」戰略的具體落地。

依託內地協同 提升亞太區域競爭力

第六,全新黃金交易中心將全面提升香港在亞太地區的綜合競爭力,穩固全球金融樞紐地位。過往坊間關於滬港黃金市場互相競爭的討論已告一段落,黃金中央結算系統的搭建與營運,充分體現滬港協同發展。配合北部都會區重點發展AI與科研產業,再加全新黃金交易基建,香港完成全新戰略定位,成為亞洲乃至全球兼具靈活性、協同性與競爭力的國際城市。

第七,維持香港一國兩制符合內地長遠發展利益。海外評論往往片面聚焦一國兩制的政治層面,忽略香港辯證式的發展特徵:一方面,香港的制度發展須配合中央國家安全戰略;另一方面,市場導向、規劃持續完善的本地經濟,為國家經濟現代化、人民幣國際化承擔不可替代的功能。

香港黃金中央結算交收系統的設立,具重大經濟與戰略意義。經濟層面,鞏固香港全球金融中心地位,提升亞太及全球市場競爭力;該系統亦是中央五年規劃下香港整體產業布局的重要一環。

Hong Kong's Gold Central Clearing System and its significance

The launch of a gold central clearing and settlement system, which is conducted on a trial run basis, will have important implications for the development of the Hong Kong Special Administrative Region (HKSAR), especially since it is formulating the first five-year plan for the territory.

According to the Hong Kong government’s information, the gold central clearing and settlement system will be characterised by not only a move to roll out an initial stage of “Delivery Connect with the Shanghai Gold Exchange,” but also the inception of a new HAU price ticker designed to “furnish a specific reference rate tailored for Hong Kong” (Government Press Release, July 7, 2026).

There are plans to expand the gold storage capacity and refining capabilities, diversify gold investment products, explore the idea of using tax incentives, coordinate with insurance arrangements, consolidate the flexibility of Mandatory Provident Fund investments in gold exchange-traded funds, and institutionalise the formation of an industry-wide trade association.

Financial Secretary Paul Chan said explicitly that the National 15th Five-Year Plan has expressed its support for Hong Kong to establish a commodity trading ecosystem. By implication, the launch of the gold central clearing and settlement system in the HKSAR can be seen as a swift response from the local government to the central government’s planning and expectation. Chan remarked on July 7: “The commencement of the trial operation of the gold central clearing and settlement system today marks a significant step forward in developing Hong Kong’s gold trading infrastructure” (Government Press Release, July 7, 2026). He added that the gold trading ecosystem will enrich the depth and breadth of the financial markets in Hong Kong, generating more opportunities for local and overseas investment and opening another new chapter for the continuous prosperity of the financial sector.

Building infrastructure for a scalable gold platform

Echoing Chan’s remarks, Secretary for Financial Services and the Treasury Christopher Hui added that the HKSAR government’s vision is to construct a “scalable” and yet “integrated” gold exchange platform with the capabilities in clearing, connectivity, price discovery, storage, risk management and insurance for both local and global investors and participants.

The new gold clearing and settlement system operates under Hong Kong Precious Metals Central Clearing Limited, which is a government-owned corporation, and it will be expected to deliver efficient and credible services for gold transactions. The operation is governed by a Clearing Rulebook, according to the government’s press release. A central ledger has been set up to record the activities of settlement, the transfer of gold, the balances of participative banks, and the facilitation of gold deposits and withdrawals. The eligible gold for settlement is composed of four-hundred-ounce fine troy bars that conform with international standards.

Eleven banks have been involved in the gold clearing system, including the Agricultural Bank of China’s Hong Kong branch, ANZ, Bank of China (Hong Kong), China Construction Bank (Asia), Citi Hong Kong, ICBC (Asia), JPMorgan Chase, Standard Chartered Hong Kong, HSBC and UBS (South China Morning Post, July 8, 2026).

Chief Executive John Lee said at the Hong Kong FIC and Bond Connect Summit that the government-owned Hong Kong Precious Metals Central Clearing Limited will offer comprehensive gold services, and that the initial gold deposits and the first transaction settlements had already been completed (Hong Kong Standard, July 7, 2026). These settlements embraced many companies and their clients, ranging from mining companies to refiners, from jewellers to investors.

Expanding connectivity and investment channels with the mainland

Lee emphasised that the establishment of the gold central clearing system is attributable to the support and collaboration among the Hong Kong government, the Shanghai Gold Exchange and the eleven financial institutions on the Central Clearing Limited Board.

The Chief Executive also remarked that the first phase of Delivery Connect was conducted in partnership with the Shanghai Gold Exchange, which is a streamlined platform for participants to use gold holdings to settle their transactions in Hong Kong and Shanghai markets (Hong Kong Standard, July 7, 2026). According to John Lee, three banks had already been participating in this Connect initiative and two-way transfer could be completed.

The Summit attended by John Lee witnessed the participation of Pan Gongsheng, the governor of the People’s Bank of China (South China Morning Post, July 8, 2026). He unveiled several policy enhancements, including a sixty per cent increase in the investment quota for the Bond Connect’s southbound segment and the diversification of the Chinese bonds products. These measures expand investment channels and can be seen as “gifts” from the central government to Hong Kong after the 29th anniversary of its return to the motherland. Pan added that the annual net investment quota under the Bond Connect scheme would be increased to eight hundred billion yuan from the current five hundred billion yuan. Moreover, China’s foreign exchange reserves will continue to increase their asset allocation in the HKSAR, thereby stimulating Hong Kong’s capital market development.

The Hong Kong Exchanges and Clearing has also revitalised its US dollar gold futures contract, and it is planning to develop a new yuan gold futures contract with the support from the Shanghai Gold Exchange. Furthermore, HAU as a new gold price ticker has been introduced in collaboration with Bloomberg for the purposes of gold trading and settlement in the HKSAR.

Strengthening Hong Kong as a super-connector for commodity trading

At the same time, the Hong Kong Monetary Authority’s chief executive Eddie Yue, witnessed the signing of a Memorandum of Understanding between the Hong Kong Exchange and Clearing Limited and the Cross-Border Interbank Payment System, which is a primary channel for cross-boundary yuan payments and clearing under the People’s Bank of China. This new understanding is economically significant, because it can accelerate the development of fixed income and currency in Hong Kong and consolidate the HKSAR’s role as a leading offshore Renminbi centre.

The establishment of the new gold central clearing and settlement system has important implications for the HKSAR and its relations with the central government, both economically and politically.

First, economically, Hong Kong’s financial and capital markets are consolidated further, offering a variety of products for overseas investors. It was reported that the government aims at expanding the gold storage capability to two thousand tonnes and to enhance cross-boundary physical gold settlement. As such, gold transactions will help Hong Kong consolidate and expand its status as one of the world’s important financial, monetary and even gold centres.

Second, the establishment of the gold clearing and settlement system is going to reposition Hong Kong as a super-connector linking with the Shanghai Gold Exchange. If Hong Kong is already a premier offshore Renminbi transaction centre for the central government in Beijing, the transactions of gold and Renminbi will be naturally accelerated.

Third, from the perspective of the political economy of development, if Hong Kong’s financial and monetary system remains an important modernisation window of China to the outside world, the addition of the gold centre is going to strengthen Hong Kong’s economic usefulness to the Chinese Mainland.

Maximising comparative advantages under one country two systems

In other words, the HKSAR remains and will remain a crucial economic conduit for China to accelerate its Renminbi internationalisation, to expand its gold transactions internationally, and to strengthen its Belt and Road Initiatives through the utilisation of financial, capital and gold platforms in Hong Kong.

Fourth, as mentioned explicitly by Paul Chan, the launch of the gold clearing and settlement system in Hong Kong speaks to the central government’s Five-Year Plan, which expects more economic contributions from the HKSAR and which hopes that Hong Kong can expand its commodity trading ecosystem. By implication, the “one country, two systems” of Hong Kong is going to prosper further by fully utilising the comparative advantages of the HKSAR’s legal system, financial and monetary centre, and the newly established gold clearing and settlement centre.

Fifth, in recent years, as the central government has been encouraging the HKSAR to play a more proactively external role, like the establishment of the International Organisation for Mediation and the visits of the HKSAR leaders to foreign countries in Central Asia and the Middle East to seek foreign direct investment, it is clear that Beijing has been unleashing the legal and economic potential of Hong Kong to the full extent. In other words, the market-led economic system in Hong Kong’s “one country, two systems” is being utilised by the central government to connect the HKSAR with both the external world and internal Chinese cities, such as Shanghai Gold Exchange in the case of the establishment of Hong Kong’s gold clearing and settlement centre. The objective of strengthening Hong Kong’s “external connections and internal communications” can be achieved by the establishment of this new gold centre in the HKSAR.

Enhancing regional competitiveness through mainland collaboration

Sixth, the setting up of this new gold centre will strengthen Hong Kong’s economic competitiveness in the Asia Pacific region. The status of Hong Kong as a global financial hub will be consolidated. Old debates over Hong Kong and Shanghai competing have ended. Instead, Shanghai and Hong Kong have been collaborating well in the establishment and operation of the Hong Kong gold clearing and settlement system. With the advancement of the Northern Metropolis, emphasising Artificial Intelligence and scientific research, alongside the establishment of a new gold clearing and settlement centre, Hong Kong is strategically repositioning itself as a dynamic, adaptive, collaborative, and competitive city, both within Asia and globally.

Seventh, it is crystal clear that it is in the interest of the Chinese Mainland to maintain the “one country, two systems” in Hong Kong. Foreign critics of the “one country, two systems” have unduly focused on the political aspect of development, but they have neglected a dialectical development in the HKSAR: on the one hand, its political development has to be reshaped and realigned with the national security needs of the central government, but on the other hand, its market-led and increasingly better planned economy is playing a crucial role for China’s persistent economic modernisation and internationalisation of yuan.

In conclusion, the establishment of Hong Kong’s gold clearing and settlement system is economically and politically significant. Economically, Hong Kong’s role as a global financial centre is going to be strengthened further. Its economic competitiveness in Asia and the world is expected to be buttressed; the gold clearing and settlement system is part of the more comprehensive planning of Hong Kong amid the central government’s Five-Year Plan.

Driving the long-term strategy for financial market revitalization

The new gold clearing system is part and parcel of the Hong Kong repositioning strategy, which embraces other aspects, including the faster development of the Northern Metropolis with Artificial Intelligence and scientific research as its foci, the establishment of the International Organisation of Mediation with the usage of Hong Kong’s common-law advantage for the Chinese Mainland to strengthen its legal relations with countries along the Belt and Road Scheme, and the central encouragement of Hong Kong’s leaders to reach out to Middle East, European and Central Asian countries to expand the HKSAR’s soft power.

Clearly, the repositioning and revitalisation of Hong Kong’s financial, monetary, capital and gold markets are an indispensable part of the Chinese Mainland’s planning and strategy of utilising the “two systems” in the “one country, two systems” to the full extent, especially as the HKSAR remains market-led amid a better planned government, and as China remains a state-led socialist economy with incremental but cautious marketisation.

原刊於澳門新聞通訊社(MNA)網站,本社獲作者授權轉載。(原文按此)