2026年三種結構性力量的匯流──伊朗衝突及其對美元計價能源貿易的干擾、中國加速脫離化石燃料的轉型,以及石油人民幣發揮槓杆作用的有限窗口──為香港創造了一個既非凡且具時效性的戰略機遇。

香港目前處理全球超過75%的離岸人民幣結算(註1),並透過 mBridge(多邊央行數位貨幣橋)和Ensemble等平台建立了強大的數位金融基礎設施。然而,香港的全部潛力尚未實現,特別是在大宗商品融資、海事保險、碳市場以及人民幣結算貿易的實體基礎設施方面。

筆者認為,香港必須在四大戰略支柱上果斷採取行動,包括石油人民幣與大宗商品融資、綠色金融與碳市場、數碼金融基礎設施以及一帶一路融資,以鞏固其作為新興多極金融秩序中不可或缺的離岸樞紐角色。 採取行動的窗口期大約是在2024至2032年;此後隨着中國對石油進口的依賴程度下降,實施石油人民幣戰略的必要性將減弱,香港獨有的槓杆作用也隨之消失。

香港當前地位:主導但仍不完整

離岸人民幣樞紐

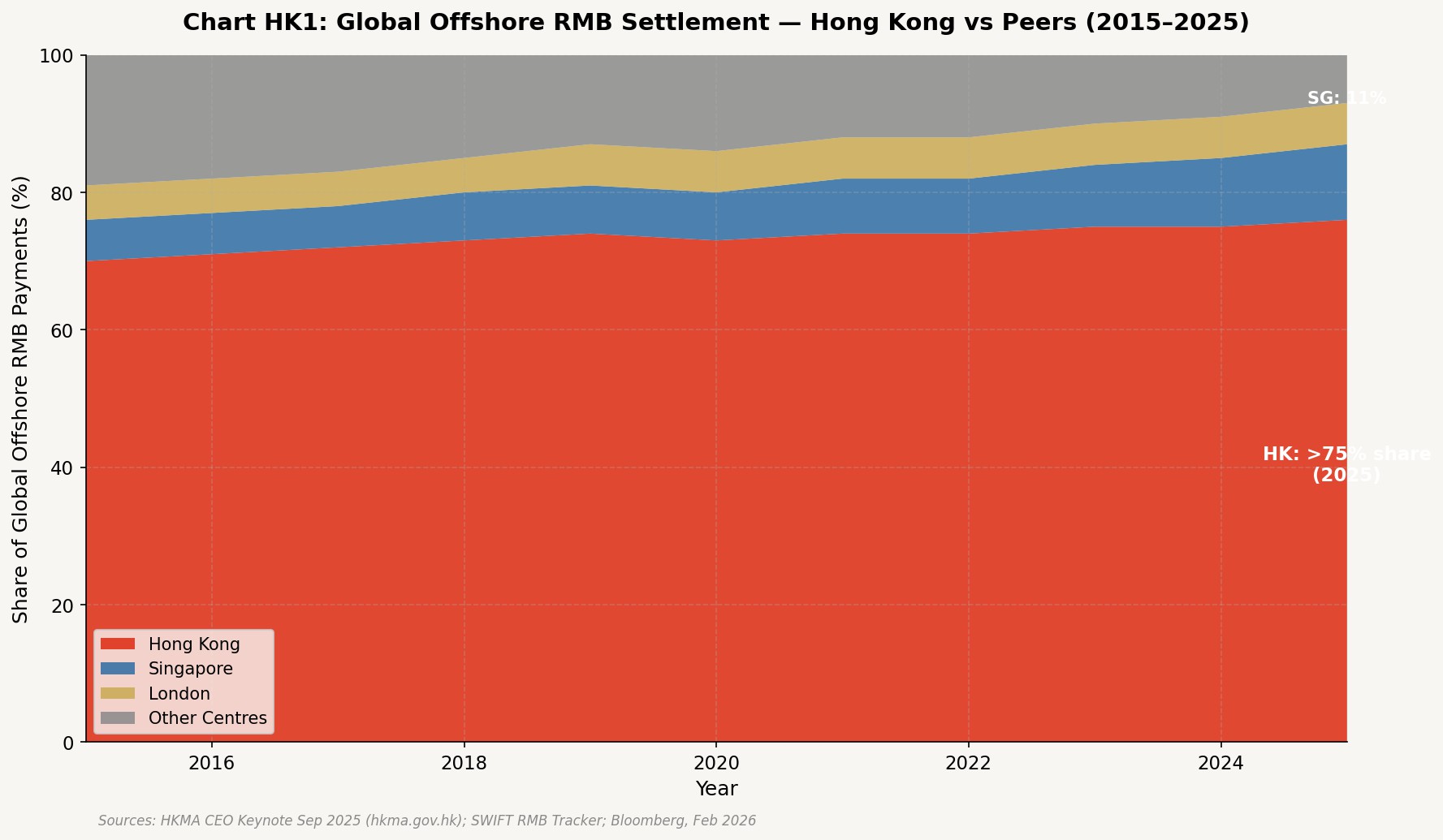

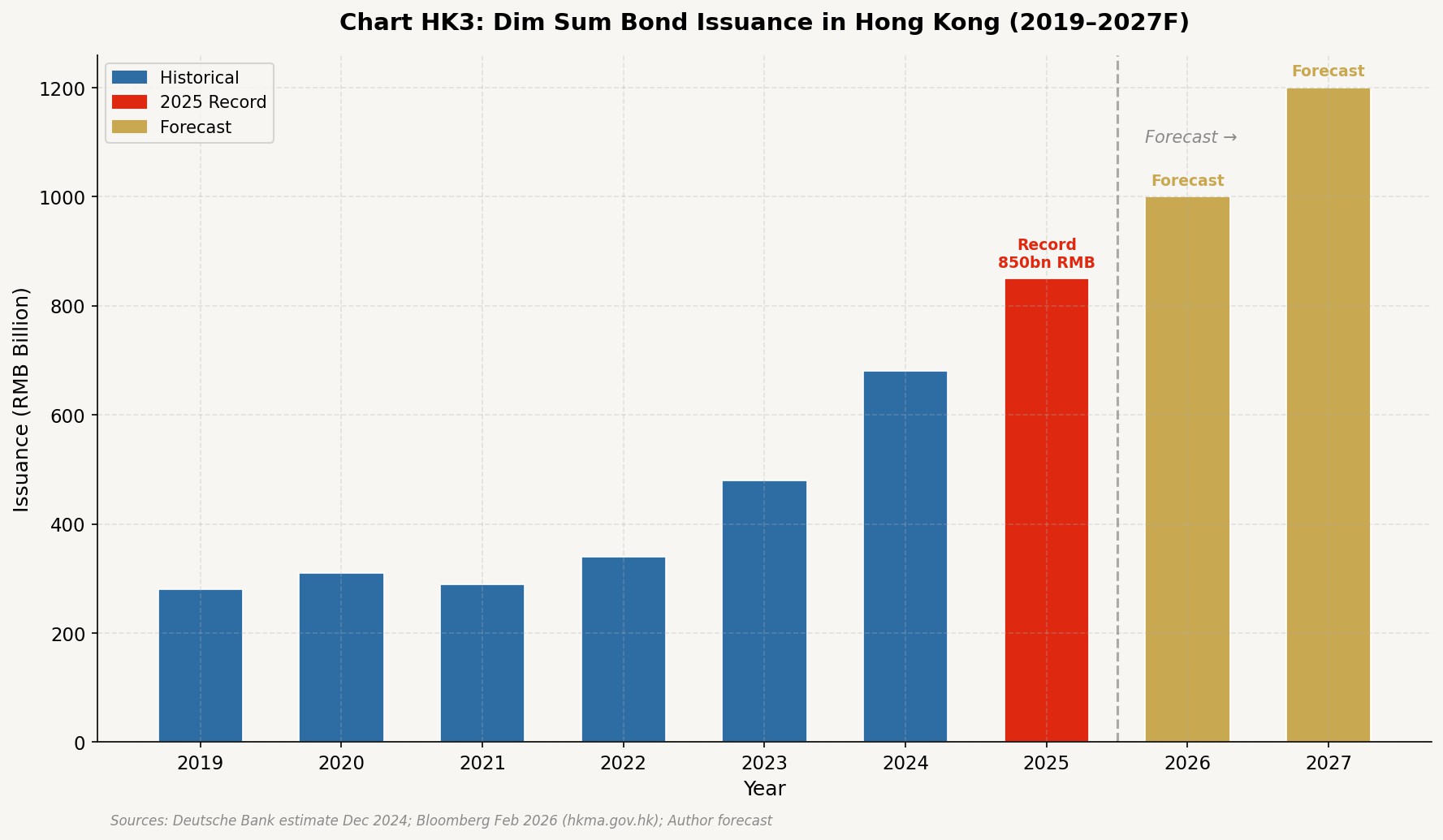

香港在離岸人民幣領域的主導地位毋庸置疑。儘管新加坡努力縮小差距,香港仍處理全球四分之三以上的離岸人民幣支付,這一比例自 2015年以來保持穩定,甚至略有增長(註1、2)。2024年經由香港結算的人民幣貿易額達到15萬億元人民幣,較2022年增長60%(註1)。香港金融管理局於2026年1月將人民幣流動資金安排增加一倍至2000億元,擴展至東盟、中東和歐洲的40家銀行(註3)。「點心」債券發行量在2025年上半年飆升至破紀錄的1.27萬億元人民幣(註1)。

數位金融架構

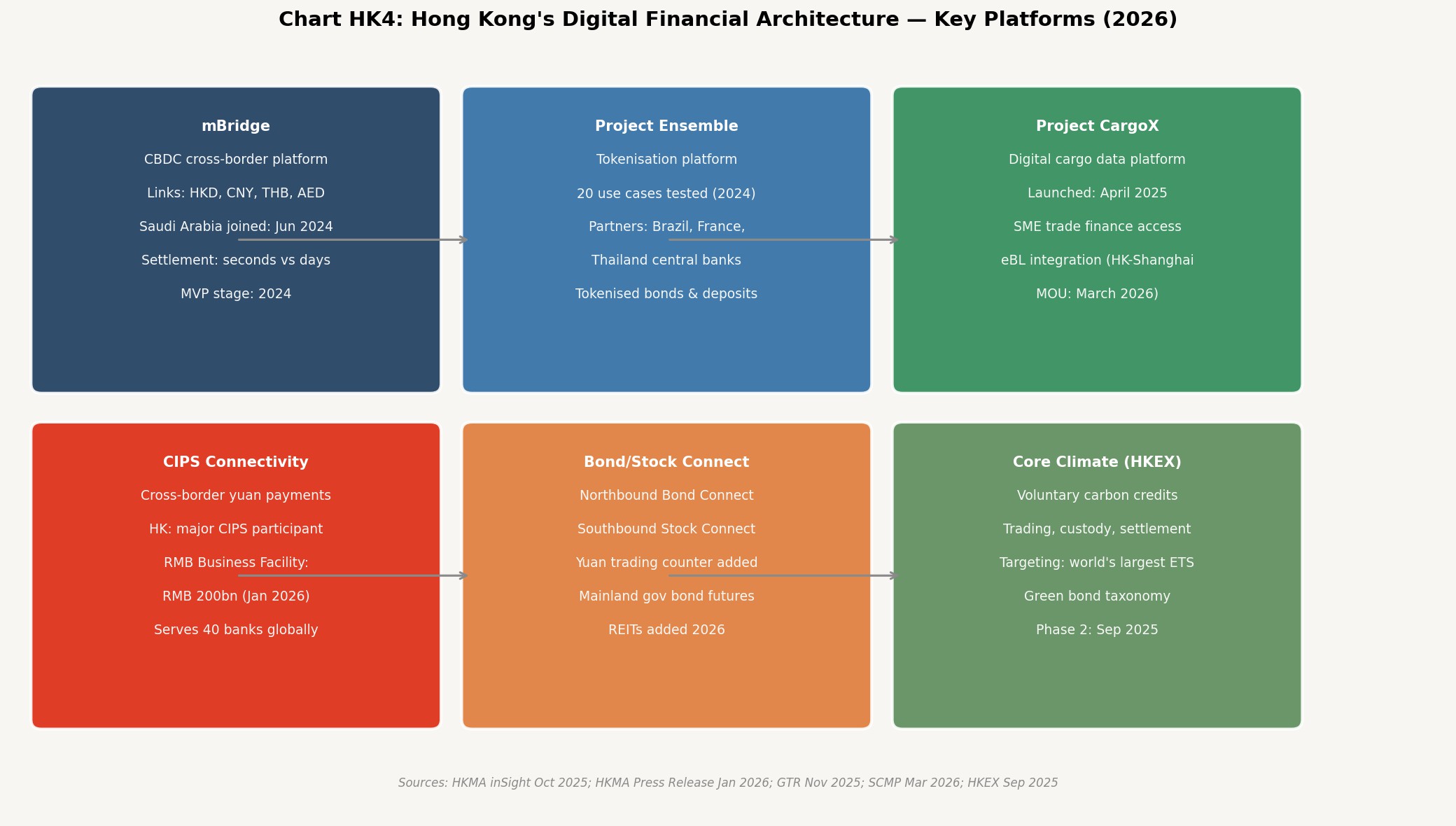

香港已建立了一個精密且互聯的數位金融生態系統。mBridge跨境央行數碼貨幣(CBDC)平台於2024 年進入最簡可行產品(MVP)階段,將數碼港元(e-HKD)與中國、泰國和阿聯酋的數位貨幣連接,將跨境結算時間從數天縮短至數秒。沙特阿拉伯於2024年6月加入該平台(註5)。同年啟動的Ensemble項目與巴西、法國和泰國的央行合作,測試了20個代幣化應用案例,涵蓋代幣化債券、存款和貿易融資工具(註5)。

金管局於2025年4月啟動CargoX項目,將貨運數據數位化,以簡化銀行流程並改善中小企業獲得貿易融資的途徑。香港與上海於2026年3月簽署合作備忘錄,將此擴展至電子提單(eBL)和基於區塊鏈的貨運數據共享(註6),更是一個里程碑。

綠色金融

2024年香港的綠色及可持續債務市場規模超過840億美元(註7),政府至今已發行等值約2500億港元的綠色債券。港交所的Core Climate平台提供自願碳信用交易、託管和結算,而該市於2025年9月發布的第二階段《可持續金融分類目錄》引入了「轉型活動」類別,與中國自身的轉型金融框架對接(註8)。綠色和可持續金融跨機構督導小組的2026至2028年戰略重點明確,在於擴大轉型金融規模並深化香港的可持續金融生態系統(註9)。

大宗商品交易與航運

香港的大宗商品交易基礎設施與新加坡和杜拜相比,差距顯著。金融發展局於2025年11月發布報告,建議香港發展實體大宗商品交易、貿易融資及避險能力,優先發展鐵礦石、銅、黃金,以及關鍵的石油和液化天然氣(LNG)(註10)。倫敦金屬交易所(LME)於2025年1月批准香港為倉儲地,到2025年7月已有八個LME認證倉庫投入運作。然而,香港缺乏石油和LNG期貨合約,這些目前仍由上海國際能源交易中心(INE,人民幣計價)以及芝加哥商品交易所/洲際交易所(CME/ICE,美元計價)主導。

戰略機遇矩陣

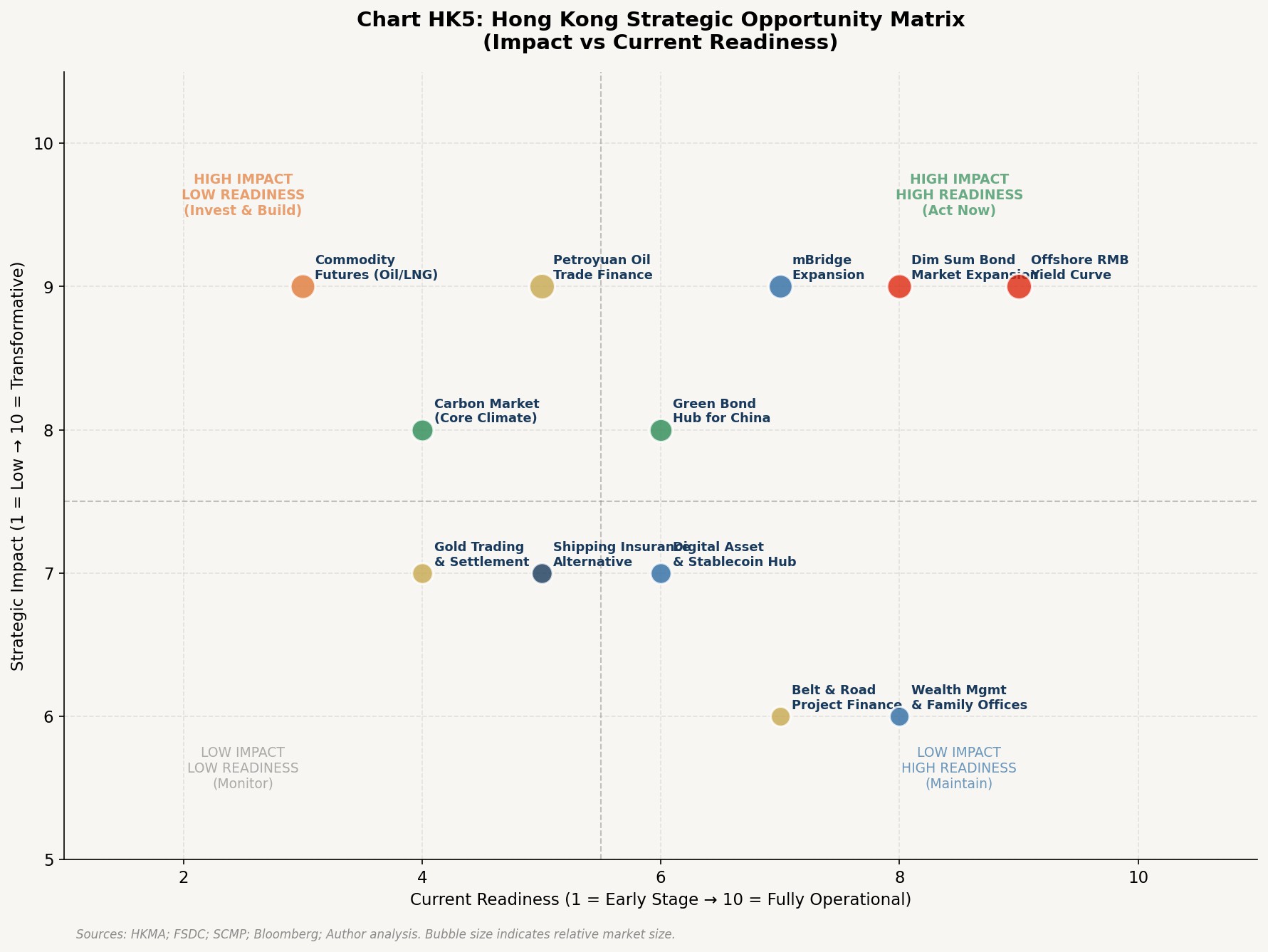

香港現有的12個關鍵機遇,可以分為兩個維度來看:潛在的戰略影響、以及香港當前的就緒程度。

第一支柱:石油人民幣與大宗商品融資──核心使命

這是最緊迫且影響力最高的支柱。伊朗危機以任何沙盤推演都無法達到的清晰度,暴露了以美元計價、西方承保的能源貿易的脆弱性。倫敦勞合社(Lloyd's of London)及船東互保協會(P&I Clubs)退出霍爾木茲海峽的戰爭風險保險,已導致西方商業油輪停航,而在中國人保(PICC)承保下營運的中國籍船隻則繼續通行。這正是2009年北京石油供應中斷推演所識別出的關鍵漏洞——而中國在推演隨後16年裏一直在為此做準備。

建立完整的離岸人民幣收益率曲線:市場缺乏最關鍵的基礎設施,是從短期(3個月票據)到長期(30年債券)完整、具流動性的離岸人民幣收益率曲線。若無此曲線,就無法有信心地為人民幣計價的貸款、債券或衍生品定價,國際投資者也無法管理人民幣資產的存續期風險。香港應在18個月內發行至少五個基準期限,每個期限最少500億元人民幣以確保流動性(註2)。

將點心債券擴展至中東及一帶一路發行商:2025年上半年破紀錄的1.27萬億元點心債券發行量,主要由中國企業以及日益增多的歐洲和亞洲發行商驅動(註1)。下一個前沿是中東,沙特阿美(Saudi Aramco)、阿布扎比國家石油公司(ADNOC)以及海灣阿拉伯國家合作委員會(GCC)的主權財富基金是天然的發行商,他們透過向中國出售石油獲得人民幣,並需要一個具流動性的市場來部署這些資金。香港應提供專門的發行支持,包括稅務優惠和簡化的監管審批,以吸引這些發行商。

啟動人民幣計價石油貿易融資:香港的銀行和貿易融資基礎設施是世界一流的,但過度傾向於美元交易。金管局於2025年1月啟動的人民幣貿易融資計劃是進一步建設的基礎。當務之急是建立大規模、專屬的人民幣流動性設施,為石油和LNG運輸提供融資,並與主要大宗商品交易商及中國國有石油公司合作,將其貿易融資業務轉移至香港。

建立大宗商品期貨市場(石油和 LNG):這是香港最顯著的結構性差距,也是其最重要的中期投資。若沒有人民幣計價的石油和LNG期貨合約,實體貿易就沒有避險機制,石油人民幣將僅維持作為結算貨幣,而非定價貨幣。香港應與上海國際能源交易中心談判,建立連結或共同掛牌的合約,允許國際參與者透過香港的法律和監管框架交易人民幣計價的石油期貨。

創建航運保險替代方案:2009年北京的沙盤推演將西方對海事保險的控制視為關鍵瓶頸。2026年的伊朗危機使這一漏洞變得具體。香港應建立香港海事保險設施(HKMIF)──這是一個由政府、中國人保及香港主要金融機構組成的公私營合作夥伴關係,為通過關鍵咽喉要道的船隻提供戰爭風險和保賠險(P&I)覆蓋,並以離岸人民幣(CNH)結算保費和理賠。

第二支柱:綠色金融與碳市場──長期布局

中國的能源轉型是未來十年重塑全球大宗商品市場最重要的結構性力量。正如國際能源總署(IEA)在2025年3月所證實,中國交通燃料的石油需求已經達到平台期(註3)。到2030年,中國的電動車隊預計將減少每日380萬桶的石油需求(註12)。這一轉型創造了巨大的融資需求──IEA估計中國在2025至2035年間需要投資約6萬億美元於清潔能源基礎設施,而香港是引導國際資本進入這項投資的天然離岸樞紐。

成為中國的綠色債券樞紐:香港應向北京尋求正式授權,成為所有主要國企和省級綠色債券的首選離岸發行地。這將集中流動資金,在香港法律下標準化文件,並創建一個深厚的、國際化的綠色債券市場。 香港現有的綠色債券框架及其包含轉型活動的第二階段分類目錄提供了監管基礎(註9)。

規模化Core Climate碳市場:香港應協商將Core Climate與中國全國碳排放交易體系(ETS)直接連結起來,允許國際資本透過香港參與中國碳市場,這將立即使香港成為全球交易量最大的碳交易樞紐(註8)。

第三支柱:數位金融基礎設施──技術賦能者

香港的數位金融平台已處於世界領先地位。 現在的重點是將其規模化並連接成一個無縫的人民幣計價國際支付和結算系統,作為SWIFT、美元架構的真實替代方案。

將mBridge擴展至所有一帶一路及海灣阿拉伯國家合作委員會(GCC)國家:mBridge平台在2024年6月擴展至沙特阿拉伯是一個重要里程碑(註5),下一階段應瞄準海合會全體六個成員國、東盟十國及非洲主要的一帶一路夥伴,創建一個完全繞過SWIFT的實時、低成本支付走廊。

推出受監管的離岸人民幣(CNH)支持穩定幣。 2026至27年度《財政預算案》公布的穩定幣發行人發牌制度,應優先敲定並推出(註2)。一個在香港法律下發行的受監管、由CNH支持的穩定幣,將成為數位金融生態系統中的關鍵結算資產,特別是用於代幣化貿易融資工具及mBridge網絡內的跨境支付。

第四支柱:一帶一路融資與財富管理

成為一帶一路項目融資樞紐:香港可以提供在香港法律下架構、由國際機構評級並向全球投資者群體聯合提供的一帶一路項目債券。這將提高一帶一路項目的可融資性和透明度,減輕中國的主權資產負債表風險,並為香港金融業產生顯著的費用收入。

擴展財富管理及家族辦公室服務:香港擁有超過3300家單一家族辦公室(註2),代表在港財富管理活動顯著且持續增長。下一個重點是吸引海灣國家的主權財富基金和家族辦公室,他們的石油人民幣收入將需要管理和投資。香港結合普通法、低稅率和深厚的資本市場,使其成為海合會財富管理相較於新加坡的自然選擇。

競爭格局:香港、新加坡、杜拜

香港相較於兩個主要競爭對手的優勢是真實的,但並非永久。下表總結了六大戰略支柱的競爭地位:

| 戰略支柱 | 香港 | 新加坡 | 杜拜(DIFC) |

|---|---|---|---|

| 離岸人民幣結算 | 主導(>75% 份額) | 增長中(11%) | 初步發展 |

| 數位金融基礎設施 | 領先(mBridge, Ensemble) | 強大(Project Orchid) | 發展中 |

| 綠色金融 | 強大(2024年840億美元) | 強大(2024年 650億美元) | 快速增長 |

| 大宗商品期貨 | 疲弱(無石油/LNG期貨) | 強大(SGX鐵礦石、 LNG) | 增長中 (DGCX) |

| 戰略支柱 | 香港 | 新加坡 | 杜拜(DIFC) |

|---|---|---|---|

| 航運保險 | 疲弱 | 強大(有互保協會進駐) | 發展中 |

| 一帶一路融資 | 強大(法律框架) | 中等 | 增長中 |

上圖明確了香港須在哪些戰略下工夫。香港在每個支柱的潛力都超過其當前表現,並且在六個支柱中的四個顯示其潛力明顯強於新加坡。現狀與潛力之間的最大差距在大宗商品交易和航運保險方面──這是2026年伊朗危機創造最緊迫,且機遇最明顯的兩個領域。

時效有限的窗口

從2024到2032年,香港大約有6到8年的有限窗口期,讓我們鞏固作為石油人民幣時代不可或缺離岸樞紐的角色。這個窗口期長短由石油人民幣的槓杆作用何時能最大化來決定,期間中國對進口石油的依賴程度高到足以賦予其強大的議價能力,要求以人民幣結算,同時中國自2009年以來建立的替代金融基礎設施,已足夠成熟來支撐運作。

窗口期之後,隨着中國的電動車轉型消除其結構性依賴進口石油,石油人民幣作為地緣政治工具的重要性將降低,建設人民幣計價金融基礎設施的緊迫性也將減弱。

香港必須以一種在其文化中並不常見的戰略來採取行動。本文提出的12項建議並非同樣緊迫;立即優先要做的,包括建立完整的離岸人民幣收益率曲線、將mBridge擴展至海合會及一帶一路國家、啟動人民幣計價石油貿易融資,這些可以且應該在12到18個月內實施。中期要在兩至四年時間內,投資在大宗商品期貨、航運保險及碳市場連結,這將定義香港在隨後十年的國際地位。這些建議不僅鞏固香港金融中心的地位,更是在新的世界秩序下金融架構的藍圖。

Seizing the Moment: Hong Kong's Strategic Blueprint for the Petroyuan Era

The confluence of three structural forces in 2026 — the Iran conflict and its disruption of dollar-denominated energy trade, China's accelerating transition away from fossil fuels, and the finite window of peak petroyuan leverage — creates a strategic opportunity for Hong Kong that is both exceptional and time-limited. The city already handles more than 75% of global offshore RMB settlements [1] and has built a formidable digital finance infrastructure through platforms such as mBridge and Project Ensemble. Yet the full potential of Hong Kong's position remains unrealised, particularly in commodity finance, marine insurance, carbon markets, and the physical infrastructure of yuan-settled trade.

This paper argues that Hong Kong must act decisively across four strategic pillars — Petroyuan and Commodity Finance, Green Finance and Carbon Markets, Digital Financial Infrastructure, and Belt and Road Financing — to cement its role as the indispensable offshore hub for the emerging multipolar financial order. The window for doing so is approximately 2024 to 2032, the period of peak petroyuan leverage. After that window, as China's oil import dependency declines, the structural imperative for the petroyuan strategy will diminish, and with it Hong Kong's unique leverage.

Hong Kong's Current Position: Dominant but Incomplete

The Offshore RMB Hub

Hong Kong's dominance in offshore RMB is not in question. The city handles more than three-quarters of all global offshore yuan payments, a share that has held steady and even grown slightly since 2015 despite Singapore's efforts to close the gap. [1] [2] RMB trade settlement through Hong Kong reached RMB 15 trillion in 2024, a 60% increase from 2022. [1] The HKMA doubled its RMB Business Facility to RMB 200 billion in January 2026, extending liquidity support to 40 banks across ASEAN, the Middle East, and Europe. [3] Dim sum bond issuance soared to a record RMB 1.27 trillion in the first half of 2025. [1]

The Digital Finance Architecture

Hong Kong has built a sophisticated and interconnected digital finance ecosystem. The mBridge CBDC platform reached MVP stage in 2024, linking the e-HKD with the digital currencies of China, Thailand, and the UAE, reducing cross-border settlement times from days to seconds.

Saudi Arabia joined the platform in June 2024. [5] Project Ensemble, launched in the same year, tested 20 tokenisation use cases in collaboration with the central banks of Brazil, France, and Thailand, covering tokenised bonds, deposits, and trade finance instruments. [5] Project CargoX, launched by the HKMA in April 2025, digitalises cargo data to streamline bank processes and improve SME access to trade finance. A landmark MOU signed between Hong Kong and Shanghai in March 2026 extended this to electronic Bills of Lading and blockchain-based cargo data sharing. [6]

Green Finance

Hong Kong's green and sustainable debt market surpassed US$84 billion in 2024 [7] and the government has issued approximately HK$250 billion equivalent in green bonds to date. The HKEX's Core Climate platform provides voluntary carbon credit trading, custody, and settlement, and the city's Phase 2 Sustainable Finance Taxonomy, published in September 2025, introduced a 'Transition Activity' category that aligns with China's own transition finance framework. [8] The Cross-Agency Steering Group's 2026–28 strategic priorities explicitly target the scaling of transition finance and the deepening of Hong Kong's sustainable finance ecosystem. [9]

Commodity Trading and Shipping

Hong Kong's commodity trading infrastructure remains its most significant gap relative to Singapore and Dubai. The Financial Services Development Council published a detailed report in November 2025 recommending that Hong Kong develop physical commodity trading, trade finance, and hedging capacity, with priority given to iron ore, copper, gold, and — critically — oil and LNG. [10] The London Metal Exchange approved Hong Kong as a warehouse location in January 2025, with eight LME-certified warehouses operational by July 2025. However, Hong Kong lacks oil and LNG futures contracts, which remain dominated by the Shanghai International Energy Exchange (INE) for yuan-denominated instruments and by CME/ICE for dollar-denominated ones.

The Strategic Opportunity Matrix

The twelve key opportunities available to Hong Kong can be mapped against two axes: their potential strategic impact and Hong Kong's current readiness to execute. This framework drives the prioritisation of recommendations in this paper.

The matrix generates a clear strategic hierarchy. Three areas demand immediate action because Hong Kong is already well-positioned and the impact is transformative: the offshore RMB yield curve, Dim Sum bond market expansion, and mBridge expansion. Three areas require significant investment to build from a low base but offer transformative returns: commodity futures, shipping insurance, and the carbon market. The remaining six areas are important but either less urgent or more incremental in their impact.

Pillar 1: Petroyuan and Commodity Finance — The Core Mandate

This is the most urgent and highest-impact pillar. The Iran crisis has exposed the vulnerability of dollar-denominated, Western-insured energy trade with a clarity that no simulation ever achieved. The withdrawal of Lloyd's of London and the major P&I clubs from war risk coverage in the Strait of Hormuz has halted Western commercial tanker traffic, while Chinese-flagged vessels operating under PICC coverage continue to transit. This is the precise scenario that the 2009 Beijing petroleum disruption exercise identified as a critical vulnerability — and that China spent the subsequent sixteen years preparing for.

Establish a Complete Offshore RMB Yield Curve. The single most critical piece of missing market infrastructure is a complete, liquid offshore RMB yield curve from the short end (3-month bills) to the long end (30-year bonds). Without this, it is impossible to price yuan-denominated loans, bonds, or derivatives with confidence, and international investors cannot manage duration risk in yuan assets. Hong Kong should target issuing at least five benchmark tenors within 18 months, with a minimum of RMB 50 billion per tenor to ensure liquidity. [2]

Expand Dim Sum Bonds to Middle East and BRI Issuers. The record RMB 1.27 trillion in Dim Sum bond issuance in the first half of 2025 was driven primarily by Chinese corporates and a growing number of European and Asian issuers. [1] The next frontier is the Middle East. Saudi Aramco, ADNOC, and the sovereign wealth funds of the GCC are natural issuers: they receive yuan from oil sales to China and need a liquid market in which to deploy those funds. Hong Kong should offer dedicated issuance support, including tax incentives and streamlined regulatory approval, to attract these issuers.

Launch Yuan-Denominated Oil Trade Finance. Hong Kong's banks and trade finance infrastructure are world-class, but they are overwhelmingly oriented towards dollar-denominated transactions. The HKMA's yuan trade finance scheme, launched in January 2025, is a foundation on which to build. The immediate priority is to create large-scale, dedicated yuan liquidity facilities for financing oil and LNG shipments, partnering with major commodity traders and Chinese NOCs to shift their trade finance operations to Hong Kong.

Build a Commodity Futures Market (Oil and LNG). This is Hong Kong's most significant structural gap and its most important medium-term investment. Without yuan-denominated oil and LNG futures contracts, there is no hedging mechanism for physical trade, and the petroyuan will remain a settlement currency rather than a pricing currency. Hong Kong should negotiate with the Shanghai International Energy Exchange to establish a linked or co-listed contract, allowing international participants to trade yuan-denominated oil futures through Hong Kong's legal and regulatory framework.

Create a Shipping Insurance Alternative (HKMIF). The 2009 Beijing simulation identified Western control of maritime insurance as a critical chokepoint. The 2026 Iran crisis has made this abstract vulnerability concrete. Hong Kong should establish a Hong Kong Marine Insurance Facility (HKMIF) — a public-private partnership between the government, PICC, and major Hong Kong-based financial institutions — to provide war risk and P&I coverage for vessels transiting critical chokepoints, with premiums and claims settled in CNH.

Pillar 2: Green Finance and Carbon Markets — The Long-Term Play

China's energy transition is the most important structural force reshaping global commodity markets over the next decade. As the IEA confirmed in March 2025, China's oil demand for transport fuels has already plateaued. [11] By 2030, China's EV fleet will displace an estimated 3.8 million barrels per day of oil demand. [12] This transition creates an enormous financing requirement — the IEA estimates China needs to invest approximately US$6 trillion in clean energy infrastructure between 2025 and 2035 — and Hong Kong is the natural offshore hub for channelling international capital into this investment.

Become the Green Bond Hub for China. Hong Kong should seek a formal mandate from Beijing to be the primary offshore issuance venue for all major Chinese SOE and provincial green bonds. This would centralise liquidity, standardise documentation under Hong Kong law, and create a deep, internationally accessible green bond market. The city's existing green bond framework and its Phase 2 Taxonomy, which includes transition activities, provide the regulatory foundation. [9]

Scale the Core Climate Carbon Market. The transformative step would be to negotiate a direct link between Core Climate and China's national ETS, allowing international capital to participate in Chinese carbon markets through Hong Kong. This would instantly make Hong Kong the world's largest carbon trading hub by volume. [8]

Pillar 3: Digital Financial Infrastructure — The Technology Enabler

Hong Kong's digital finance platforms are already among the most advanced in the world. The priority now is to scale and connect them into a seamless, yuan-denominated international payment and settlement system that can serve as a genuine alternative to the SWIFT/dollar architecture.

Expand mBridge to All BRI and GCC Countries. The mBridge platform's expansion to Saudi Arabia in June 2024 was an important milestone. [5] The next phase should target all six GCC members, the ten ASEAN nations, and key African BRI partners, creating a real-time, low-cost payment corridor that completely bypasses SWIFT.

Launch a Regulated CNH-Backed Stablecoin. The licensing regime for stablecoin issuers, announced in the 2026-27 budget, should be finalised and launched as a priority. [2] A regulated, CNH-backed stablecoin issued under Hong Kong law would become a key settlement asset within the digital finance ecosystem, particularly for tokenised trade finance instruments and cross-border payments within the mBridge network.

Pillar 4: Belt and Road Financing and Wealth Management

Become the Belt and Road Project Finance Hub. Hong Kong can offer BRI project bonds structured under Hong Kong law, rated by international agencies, and syndicated to a global investor base. This would improve the bankability and transparency of BRI projects, reduce China's sovereign balance sheet exposure, and generate significant fee income for Hong Kong's financial sector.

Expand Wealth Management and Family Office Services. Hong Kong's 3,300+ single-family offices [2] represent a significant and growing concentration of wealth management activity. The next priority is to attract the sovereign wealth funds and family offices of the Gulf states, whose petroyuan receipts will need to be managed and invested. Hong Kong's combination of common law, low taxes, and deep capital markets makes it the natural choice over Singapore for GCC wealth management.

The Competitive Landscape: Hong Kong vs Singapore vs Dubai

Hong Kong's advantages over its two main competitors are real but not permanent. The following table summarises the competitive position across the six strategic pillars.

Strategic Pillar | Hong Kong | Singapore | Dubai (DIFC) |

Offshore RMB Settlement | Dominant (>75% share) | Growing (11%) | Nascent |

Digital Finance Infrastructure | Leading (mBridge, Ensemble) | Strong (Project Orchid) | Developing |

Green Finance | Strong (US$84bn, 2024) | Strong (US$65bn, 2024) | Fast-growing |

Commodity Futures | Weak (no oil/LNG futures) | Strong (SGXiron ore, LNG) | Growing (DGCX) |

Shipping Insurance | Weak | Strong (P&I clubs present) | Developing |

Belt & Road Financing | Strong (legal framework) | Moderate | Growing |

The radar chart makes the strategic imperative clear. Hong Kong's potential in every pillar exceeds its current performance, and in four of the six pillars, it has the potential to be significantly stronger than Singapore. The gap between current and potential is largest in commodity trading and shipping insurance — the two areas where the 2026 Iran crisis has created the most urgent and visible opportunity.

Conclusion: A Time-Limited Window

The strategic analysis presented in this paper leads to a single, clear conclusion: Hong Kong has a finite window of approximately six to eight years — from 2024 to 2032 — in which to cement its role as the indispensable offshore hub for the petroyuan era. This window is defined by the period of peak petroyuan leverage, during which China's oil import dependency remains high enough to give it maximum bargaining power in demanding yuan settlement, while the alternative financial infrastructure it has built since 2009 is mature enough to support it.

After this window, as China's EV transition eliminates its structural oil import dependency, the petroyuan will become less important as a geopolitical tool, and the urgency of building yuan-denominated financial infrastructure will diminish. Hong Kong must therefore act with a sense of strategic urgency that is not always characteristic of its regulatory culture.

The twelve recommendations in this paper are not equally urgent. The immediate priorities — establishing a complete offshore RMB yield curve, expanding mBridge to GCC and BRI nations, and launching yuan-denominated oil trade finance — can and should be implemented within 12 to 18 months. The medium-term investments — commodity futures, shipping insurance, and the carbon market link — require two to four years to build but will define Hong Kong's position for the following decade. Together, they constitute a blueprint for Hong Kong to become not merely a financial centre, but the financial architecture of the new world order.

參考文獻 References:

HKMA. (2025, September 26). Keynote Address at the Treasury Markets Summit 2025 — RMB Internationalisation Statistics. Hong Kong Monetary Authority. https://www.hkma.gov.hk/eng/news-and-media/speeches/2025/09/20250926-3/

Chuang, A. & Hung, E. (2026, February 25). Hong Kong seeks to hone edge as offshore yuan hub, digital-asset front runner. South China Morning Post. https://www.scmp.com/news/hong-kong/article/3344634/hong-kong-seeks-hone-edge-offshore-yuan-hub-digital-asset-front-runner

HKMA. (2026, January 26). HKMA Doubles Renminbi Business Facility to RMB 200 Billion. Hong Kong Monetary Authority. https://www.hkma.gov.hk/eng/news-and-media/press-releases/2026/01/20260126-3/

Bloomberg News. (2026, February 25). Hong Kong Moves to Attract More Offshore Yuan Borrowers and Expand Bond Market. Bloomberg. https://www.bloomberg.com/news/articles/2026-02-25/hong-kong-seeks-to-attract-more-borrowers-in-offshore-yuan-push

HKMA. (2025, October 30). Building Highways and Bridges for Hong Kong's Digital Economy — mBridge and Project Ensemble. HKMA CEO inSight. https://www.hkma.gov.hk/eng/news-and-media/insight/2025/10/20251030/

SCMP. (2026, March 2). Hong Kong, Shanghai sign pact on digital trade finance, cross-border data link. South China Morning Post.

https://www.scmp.com/business/banking-finance/article/3345160/hong-kong-shanghai-sign-pact-digital-trade-finance-cross-border-data-linkTransport and Logistics Bureau, HKSAR. (2025, November 18). Speech by Secretary for Transport and Logistics at the World Maritime Merchants Forum 2025. https://www.tlb.gov.hk/eng/psp/speeches/transport/2025/20251118a.html

HKEX. (2025, September 1). Carbon Credits: A Buyer's Guide. Hong Kong Exchanges and Clearing Limited. https://www.hkex.com.hk/-/media/HKEX-Market/Join-Our-Markets/Core-Climate/HKEX_Carbon-Credit-Buyers-

Guide_English_2025.pdfCross-Agency Steering Group on Green and Sustainable Finance. (2026, January 30). Strategic Priorities for 2026–2028. Sustainable Finance Hong Kong. https://www.sustainablefinance.org.hk/storage/uploads/4ce0466f-6c89-4bd7-888f-2dabd6c14f3d/CASG_2026-28-Priorities_%20en.pdf

GTR (Global Trade Review). (2025, November 12). Hong Kong maps out plans for commodity trading and finance hub. https://www.gtreview.com/news/asia/hong-kong-maps-out-plans-for-commodity-trading-and-finance-hub/

IEA. (2025, March 11). Oil demand for fuels in China has reached a plateau. International Energy Agency. https://www.iea.org/commentaries/oil-demand-for-fuels-in-china-has-reached-a-plateau

Rhodium Group. (2025, July 1). Electric Trucks and the Future of Chinese Oil Demand.

https://rhg.com/research/electric-trucks-and-the-future-of-chinese-oil-demand/